What is included in discontinued operations?

Mia Phillips

Published Jan 11, 2026

What Are Discontinued Operations? In financial accounting, discontinued operations refer to parts of a company’s core business or product line that have been divested or shut down, and which are reported separately from continuing operations on the income statement.

What is not associated with extraordinary items?

GAAP specifically stated that write-offs, write-downs, gains, or losses on the following items were not to be treated as extraordinary items:

- Abandonment of property.

- Accruals on long-term contracts.

- Disposal of a component of an entity.

- Effects of a strike.

- Equipment leased to others.

- Foreign currency exchange.

How do you calculate loss from discontinued operations?

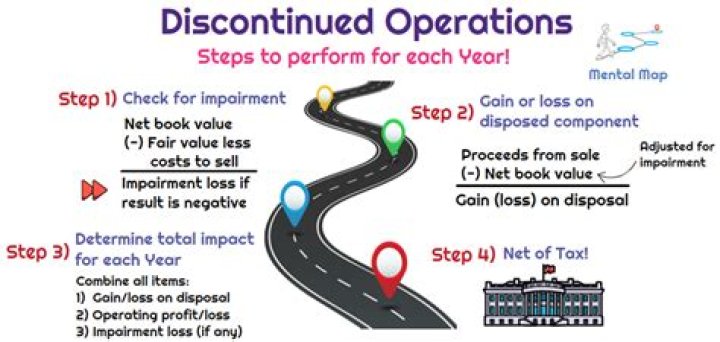

Determine the gain or loss from the disposition of the discontinued operation only if the disposal occurred within the accounting period. The gain or loss is the difference between the selling price and the fair-market value of the discontinued operation, minus transaction costs.

What are extraordinary items?

Extraordinary items were gains or losses from infrequent and unusual events that were separately classified on companies’ financial statements.

What are the examples of extraordinary items?

Examples of extraordinary items include expenses to deal with a fire, earthquake, or uninsured losses from a flood, the gain or loss from early retirement of debt, or the expropriation of a property by a foreign government.

What is the treatment of extraordinary item in different cases?

Extraordinary items were gains or losses from infrequent and unusual events that were separately classified on companies’ financial statements. FASB discontinued the accounting treatment for extraordinary items to reduce the cost and complexity of preparing financial statements.

How are extraordinary items classified on an income statement?

If an event or transaction meets the criteria for extraordinary classification, an entity is required to segregate the extraordinary item from the results of ordinary operations and show the item separately in the income statement, net of tax, after income from continuing operations.

Why do we need to eliminate the concept of extraordinary items?

2 Eliminating the concept of extraordinary items will save time and reduce costs for preparers because they will not have to assess whether a particular event or transaction event is extraordinary (even if they ultimately would conclude it is not).

What makes an event or transaction an extraordinary item?

Extraordinary Items Extraordinary items are events and transactions that are distinguished by their unusual nature and by the infrequency of their occurrence. Thus, both of the following criteria should be met to classify an event or transaction as an extraordinary item: a. Unusual nature.

How are extraordinary items eliminated from GAAP income statement?

This Update eliminates from GAAP the concept of extraordinary items. Subtopic 225-20, Income Statement—Extraordinary and Unusual Items, required that an entity separately classify, present, and disclose extraordinary events and transactions.