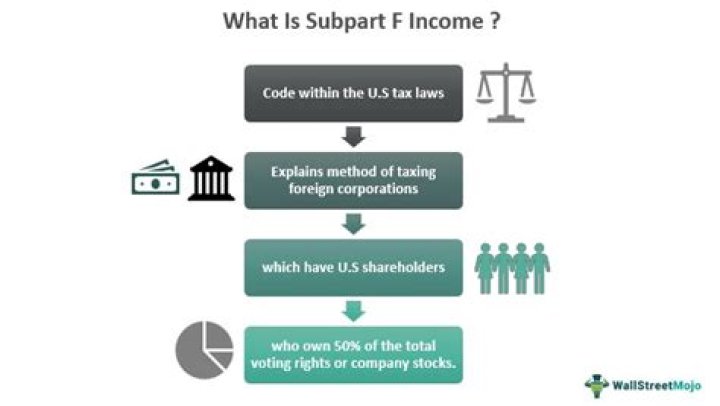

What is CFC subpart F income?

Mia Cox

Published Jan 07, 2026

To avoid this type of scenario, the U.S. enacted, in 1962, Subpart F – Controlled Foreign Corporations, which stipulates that any Subpart F income — which is income with little or no economic relation to the CFC’s country of incorporation — earned by a CFC that is not distributed or otherwise taxed for the tax year in …

How do you calculate CFCs?

A CFC is technically defined as any foreign (i.e., non-U.S.) corporation, if more than 50% of (i) the total combined voting power of all classes of stock of such corporation entitled to vote; or (ii) the total value of the shares in such corporation, is owned in the aggregate, or is considered as owned by applying …

What is a CFC charge?

As has already been noted, a CFC is a non-UK resident company that is controlled by UK resident companies and/or individuals. The CFC regime imposes a UK corporation tax liability, a ‘CFC charge’, on the corporate owners of a CFC where UK profits have been artificially diverted from the UK.

What is a CFC for tax purposes?

A controlled foreign corporation (CFC) is a corporate entity that is registered and conducts business in a different jurisdiction or country than the residency of the controlling owners. Controlled foreign corporation (CFC) laws work alongside tax treaties to dictate how taxpayers declare their foreign earnings.

What is included in Gilti income?

Generally, GILTI is foreign income earned by CFCs from intangible assets, such as copyrights, trademarks, and patents. CFCs are foreign corporations in which more than 50% of the vote or value is owned by U.S. shareholders who each own 10% or more of the CFC.

Can a CFC be taxed under Subpart F?

Under Subpart F rules and IRC 952 , U.S. shareholders of a CFC may be taxed on certain foreign corporation income, even if it has not been distributed. The income attributed to them is based on their ratable share.

What are the rules for Subpart F income?

Subpart F Income & Controlled Foreign Corporations (CFC): The IRS Rules for Subpart F Income, CFC, and U.S. Shareholder Foreign Earnings are very complicated. Essentially, Subpart F Income involves CFCs ( Controlled Foreign Corporations) that accumulate certain specific types of income (primarily passive income).

Where does CFC income go in Internal Revenue Code?

Undersubpart F (Secs. 951–964) of the Internal Revenue Code, subpart F income of a controlled foreign corporation (CFC) is included in its U.S. shareholders’ income before the income actually is distributed to the U.S. shareholders.

What is Subpart F of controlled foreign corporations?

Subpart F deals with the U.S. taxation of amounts earned by controlled foreign corporations (CFCs). It provides that certain types of income of CFCs, though undistributed, must be included in the gross income of the U.S. shareholder in the year the income is earned by the CFC.